The Impending Economic Tsunami

Please note this is a work in progress and any comments are appreciated.

Peer Review additions February 2022 shown in purple

Quick read summary

Since Homo Sapiens appeared on this planet they have been subduing it. Being sapiens they developed models for the economy which we now call GDP. In recent years there have been changes to the SNA, which is the UN document countries use to calculate GDP. I question the reliability of the global and national GDPs as measurement instruments.

It started with the bursting financial bubbles of 2008. Then added cryptocurrencies that aren’t even paper linked to economic activity. Add to that climate change. Then Covid 19. And consumption will plateau due to a population no longer expanding. We have banking instruments that are virtual and, in some cases, recursively virtual. And the SNA champions those activities. I thus perceive we are heading toward some sort of Impending Economic Tsunami!

The GDP figures are inaccurate, in part because the model has moved ‘circulation’ and ‘rents’ into ‘production’. The Classical Economic Model excluded them from 'productive'. The paper financial instruments of the world economy have become, quite literally, ‘the emperor’s new clothes’!

We live on a biosphere that was a garden and has become a city. As a garden-city we need to look carefully at the economy of the biosphere. The current economic model is based on the belief in an ever-expanding economy. But we should not see it as a ‘continuously expanding pie’ but a ‘fixed-size pie that has to be cut in such a way to allow everyone a slice’. Continual expansion cannot function in a globalised world with a static population size and recycling of resources. It won’t work.

We need to look again at the biosphere we call earth, including its human population. We need to develop a new economic model based on solid reality, not speculative virtual instruments. That model needs to be coherent so that global and national policies are implementable.

Within a closed biosphere we cannot manufacture wealth out of nothing. So countries need to see themselves as interdependent, not independent. As do individual human beings. The measure of GDP needs to be providing for the Survival and Welfare needs of every person on the planet: Some sort of Universal Basic Income (UBI). Leisure and luxury can only be provided where there is a surplus.

We need to create a new SNA: Not for a perpetually expanding GDP but a Global GDP balancing labour, energy and resources. In that SNA banking and financial services would be an intermediary, not a wealth creator. It’s not production per se that has value but humankind within this closed system biosphere!

'A healthy economy should be designed to thrive, not grow.' (Kate Raworth, author of Doughnut Economics) Doughnut Economics gives a measurement tool for ecological and social foundations and develops the core concept of a closed system biosphere. This is not about right-wing, left-wing or green politics but about a 'safe and just space for humanity'.

The whole story

How we got to where we are… and what we need to do going forward

Early Community

Early on people were hunter-gatherers and nomads. They were filling the earth, subduing it and demonstrating dominion over other living creatures. The world seemed infinitesimally large with limitless resources. Subduing it was more important than caring for it. But then people started settling down, farming and building things.

That transition meant people bartered with each other, for example ‘I’ll help you do x for a chicken’. Then people discovered gold and it was beautiful and very rare. Therefore it had intrinsic value for them. It became something with which to trade. This was a transition away from subsistence agriculture to farming that gave a surplus for trade.

Gold and Money Lending

The inputs to development are earth resources, energy and labour. Labour was either paid at subsistence level or preferably slave. Some of the huge buildings in BCE were built using slave labour. People saw earth resources as infinite although energy was limited: oil for lighting and wood for fire. It was a Malthusian Economy.

Malthusian Economy Theory

Almost all economies before the industrial revolution functioned on the Malthusian economy model. Income and life expectancy was determined by fertility and mortality at each income level. Before 1800 the improvement of production technologies resulted only in population growth. It did not give any gain in material living conditions beyond those found in hunter-gatherer societies. Population growth was limited by the food supply. Hence initially within a Malthusian economy the population grow. Then it reduces living standards to the point of triggering a population die-off.

It is only in trade of surplus that creates any wealth. Thus we move to the Mercantile Economic Theory.

Mercantile Economic Theory

Early Mercantile economic theory was that gold had inherent value. Increasing the quantity of it for the nation or leader was what increased wealth. This was true until the 18th century when people started thinking abstractly about economic theory. After the Second World War the gold standard was abolished. This created a radical shift in the world economy and the economic theories supporting it. Gold is solid and tangible. So the Mercantile Economic Theory, though limited, was coherent and thus functional.

Coinage and Banknotes

Although gold had been used for exchange, coins were only introduced around the 5th or 6th century BCE as tokens for trade. Early coins were made of an alloy of silver and gold and thus maintained the precious metal link. In China in the 2nd century BCE ‘deerskin notes’ were introduced as a predecessor of paper currency.

The introduction of coinage enabled abstract and multi-layer transactions. I could sell you something, get coins and then use some for one thing and some for another. I could also store these tokens and use them when I wanted. I could even have a third party hold those tokens on my behalf: the predecessor of banks. Value could be identified numerically according to the currency. It enabled borrowing and lending to be more accurately enumerated and thus increase.

China had used banknotes in the 13th century and to a limited extent by travellers such as Marco Polo. However, European banknotes didn’t widely appear till the 17th century. Banknotes were seen as a promissory note: A promise to pay someone in precious metals on presentation of the note. Because it removed the need to carry precious metals it became quickly and widely accepted. It was, at that stage linked directly to gold reserves held by the banks.

Early Pandemics

We have very little accurate medical information about pandemics until the 19th Century. Because vaccines and medical treatment were unavailable pandemics caused a significant death toll. This affected both the population of the world (labour resource) and the world economy significantly.

Smallpox is an example. It killed up to one-third of the population. For example, the Plague of Athens that occurred in 430 BCE. Or the Antonine Plague 165–180 CE where returning soldiers picked up the disease in Iraq and brought it home with them to Syria and Italy. Add to that the Plague of Cyprian 251–266 CE where the Roman empire stopped growing as a consequence.

Standard of living was determined not by technological progress but by the size of the population. There was a large spike in living standards early in the 14th century. Incomes increased by approximately one third in just a few years. The Black Death, a bubonic plague killed between 75 and 200 million people in Eurasia and North Africa. It peaked between 1347 and 1351. Almost half the population of England died. But those who did survive were materially much better off! Before the industrial revolution ‘the economy was a brutal zero-sum game and the death of your neighbour was to the benefit for those that did survive’.

Classical Economic Theory

|

| François Quesnay |

He separated people into three classes. They were either Productive, Manufacturers / Artisans or the ‘sterile’ class. In his thinking was the production boundary. The Productive class were only those who extracted something new from the land. These were farmers, miners, fishermen and other related jobs. Everything on the other side of the production boundary was only recycling what had been produced. He placed manufacturers or artisans, who were turning what had been produced into something useful, on the other side of the boundary. The sterile class included landlords, nobility and clergy! They were sterile since they consumed but did not offer anything in return.

|

| Anne Turgot |

His model was simplistic and a contemporary of his. Turgot, developed it further. He added artisans and even judges to administer justice, as necessary to society for value creation. He separated active landlords from those merely extracting rents and thus unproductive. There were thus three categories: wages, profits and rents.

Into this came Adam Smith, David Ricardo and Karl Marx. Smith and Ricardo were early protagonists of what we would call ‘time and motion’ specialists. They looked at ways that labour could be used within the industrial revolution to make more with less labour. The value of labour was significant to them. They wanted to reduce labour costs and increase production. Increasing production was on the ‘productive’ side of the line! Smith also put at the centre of his thinking the self-centredness of people. He believed everyone was looking for the most (financially) advantageous employment. He didn't believe anyone worked for the benefit of the community in which he lived. This he described as an ‘invisible hand’ guiding their decisions.

|

| Adam Smith |

|

| David Ricardo |

The population increase in the 18th century was modest contrasted with the latter 20th century. But this set the core principle in Classical Economic Theory. That of an ever-increasing population and ever-increasing wealth. That principle remains unchanged to this day. To that he added the principle that the scarcer the resource the higher the value it acquired.

There was one other point he introduced. This one particularly poignant to the 21st century. Capital can either be productive or unproductive. Productive capital is used to buy labour which multiplies the capital for profit. Unproductive capital is consumed on luxuries. One might think of vacation space travel this way. It does not lead to any reproduction of the capital.

|

| Karl Marx |

So we come on to the third economist, Karl Marx. Effectively he was a capitalist who believed the production should be in the hands of the workers rather than the landlords. He believed this because it was their labour in production that gave it value. This was contextually dependent on the time that they were in. He believed that the cleverness of capitalism was that it could organise production. This enabled workers to generate unprecedented amounts of surplus-value.

Because of the industrial revolution workers were no longer independent. They could not live on subsistence agriculture. They inevitably became reliant on a wage to survive. He also foresaw that capitalism is a changing beast that morphs into something new with every new era. Hence Classical Economic Theory is dynamic rather than static, while the core principles remain the same.

One could almost summarise Classical Economic Theory as this.

‘Production’ = value.

‘Rents’ = no value.

‘Banking’ = circulating value items.

What Marx failed to see was that in the dynamic evolution of capitalism Banking would be moved to production. And that rents would be redefined. So that strange anomalies would be incorporated into Economic Theory in later centuries.

Flu Pandemics

In 1918 after the First World War the world was hit with what we know as Spanish Flu. There were 500 million or more cases, killing up to 100 million people. That represented between 1% and 2.5% of the world population. At that stage medicine was less advanced and most deaths were caused by secondary bacterial infections. These could have been cured by antibiotics. Because Spanish Flu affected the young and infants the economy took a major hit.

The 1918 Flu Pandemic was by far the most devastating in recorded history. But the Russian Flu pandemic from 1889 to 1894 killed a million people. The Asian Flu of 1957-1958 killed up to 4 million people. The Hong Kong Flue of 1968-1929 killed up to 4 million people. And the Russian Flu of 1977-1979 which was caused by the same H1N1 virus as the Spanish Flu killed 700,000 worldwide.

Great Depression

|

| Wall Street Black Tuesday |

Each country tried to shore up its own economy through protectionist policies. In 1930 in the USA the Smoot-Hawley Tariff Act then precipitated retaliatory tariffs in other countries. This spiralled downwards collapsing world trade and making the depression even worse. Within four years world trade was down to one-third of the previous level.

There are contradictory views as to the cause of the Great Depression. Two of which are dominant. Milton Friedman argued that it was the banking crisis that caused one-third of banks to collapse, with knock-on effects. The Federal Reserve took no action to increase liquidity. He therefore believed what could have been a normal recession turned into the Great Depression.

|

| John Maynard Keynes |

Although Roosevelt spent some on public works and farm subsidies, he never gave up trying to balance the budget. According to Keynesian advocates it was never enough to pull the economy out of recession till the start of the Second World War.

The USA unlinked from gold standard & then others followed

The gold standard allowed countries and merchants to exchange gold as a common international currency. This was locked to the amount of gold they were holding or someone was holding on their behalf. In 1933 the USA unlinked their dollar from the gold standard. This made US dollars currency float based upon the perception people had about the economy of the country. It wasn’t fully recognised at the time but this started national economies becoming ‘virtual’. GDP would become numbers on a sheet divorced from real production in the Classical Economic Model.

The Bretton Woods system

After the Second World War when the USA was seen to be at the centre of political and economic dominance. A conference was held at Bretton Woods in the USA. At that conference the dollar was fixed at $35 per ounce and all other currencies then had adjustable rates to the dollar. Countries could impose capital controls to stimulate their economies. This would be without the historic problems they perceived from the gold standard.

This enabled countries to monitor and control external movements of the currency. From a globalised single currency (ie gold) the world moved to a segmentized competitive system. This was based on paper rather than any tangible assets. It facilitated trading in currencies. So-called fiat currencies had intrinsic though virtual value. It encouraged competition between countries rather than facilitating interdependence between them.

1948: UN Declaration of Human Rights

After the trauma of the Second World War the United Nations was formed. In 1948 the Universal Declaration of Human Rights was written. The core principle was that every human being has the right to life, liberty and security of person. This elevated human beings to the top of the pyramid of value.

Some of the key-value statements are as follows:

Article 4: No one shall be held in slavery or servitude; slavery and the slave trade shall be prohibited in all their forms.

Article 17: Everyone has the right to own property alone as well as in association with others.

No one shall be arbitrarily deprived of his property.

Article 25: Everyone has the right to a standard of living adequate for the health and well-being of himself and of his family, including food, clothing, housing and medical care and necessary social services, and the right to security in the event of unemployment, sickness, disability, widowhood, old age or other lack of livelihood in circumstances beyond his control.

Article 26: Everyone has the right to education… Parents have a prior right to choose the kind of education that shall be given to their children.

1930-2050: Vast Population Growth

Between 10,000 BCE and 1700 CE population growth was averaging around 0.04%. By 1900 it was about 0.5% but it peaked at 2.5% in 1968 dropping again to 1% by 2019. It is expected to drop to 0.1% by 2100, becoming at that stage almost a plateau.

This explosion in population growth gave an explosion of need – food, clothing, housing, energy for survival. and then services of arts, sport, vacations etc for leisure and luxury. The economic theories currently in use are based upon a ‘continually expanding pie’ (ie population). This has been true but will no longer be true by the end of this century.

The world was in some sort of ‘slash and burn’ mode in the 19th and 20th centuries. So a severe amount of damage was done to the planet resulting in what we now call ‘climate change’. Almost nobody was attributing value to the resource we call planet earth. During that era earth was seen as a limitless resource, to be plundered!

Neoclassical Economic Model

The Neoclassical Economic Model removed the objective conditions of production. It merged into it both production goods and services. It rejected Malthusian ideas on population growth seeing it now as progress. Landlords who were rent extractors were now seen as productive.

|

| Léon Walras |

The Neoclassical or Marginal Utility Theory held that all income is a reward for a productive undertaking. This overlapped with an earlier idea from Thomas Aquinas in Summa Theologia of a just price. He argued against ‘Cheating, Which is Committed to Buying and Selling’. It was a concept theologically similar to the Biblical argument against usury. Against profiteering by middlemen and moneylenders.

The introduction of calculus rather than simple arithmetic moved economics to look at marginal changes. And how they affected the quantity of product. These new theories argued that the value of things is measured in their usefulness to the consumer. Therefore there is no objective measure of value. In mass production the same applies. The marginal cost of an extra item produced on a production line is lower than the previous one.

Alfred Marshall, Professor of Political Economy at Cambridge University develop the marginal utility theory. He claimed that eventually the system comes to equilibrium in a similar way to Newton’s description of gravity. Scarcity creates the value equilibrium. Water is cheap because it is plentiful, diamonds are expensive because they are rare. This included wages; what you get is what you are worth. Thus a CEO is worth more than a doctor or nurse saving your life!

This model helped at the micro-level of how people trade. But it didn’t help at the macro level of determining the GDP or value of a country. Within that system everything except taxes went within the production boundary.

One of the core differences between classical and neoclassical economic theory is over ‘rents’. Neoclassical see rents as an equilibrium below ‘abnormal’ profits. In the classical theory ‘rents’ are income from non-produced scarce assets. For example, land but would not include patents, issuance of credit from a banking license and even legal representation. The latter being introduced in neoclassical economics. Whereas in neoclassical theory because everything is in equilibrium incomes must reflect productivity. This is almost a recursive argument within a virtual world!

The introduction of the SNA

Neoclassical Economics required a system to be developed that allowed a calculation of the value of nations. This was especially true since the gold standard had been abandoned. Trading between nations and their currencies needed a measure upon which to base that trade. This was also needed for governments to ‘steer’ the economy. Since the advent of marginality a measure of how much was actually produced became increasingly difficult to measure.

Under the neoclassical model GDP is calculated based on the value-added to industries. National accounting is based on the difference between the output cost and the consumer price. Summing all those together for the country gives you, with some minor offsets, the GDP for the country. Summing all the national GDPs gives you the GDP for the world. The value-added calculation is based on all goods and services that are sold on the market. Hence the only non-production category became government! Government should therefore be reduced to as close to zero as possible.

However, there are anomalies. Government services that affect the economy and future investment, eg R&D, care and the black or grey markets. There are further anomalies. If both me and my neighbour care for our own children this is not included in the GDP. If however we each care for the other’s children it is!

Work done in the house by a partner not working outside the house is excluded but if someone is paid to do that work then it is included. The costs included in running a bank account, union dues or club memberships, all defined as ‘welfare’, are excluded.

An economist called Simon Kuznets estimated the ‘inflated costs of urban living’ to be 20-30% of consumer expenditure. Yet it was excluded!

There were debates between economists about the equilibrium. The equilibrium which was critical to the neoclassical economic model. As a result figures got added in based on estimated figures and ‘common sense’. Common sense actually know to be fairly uncommon!

After the Second World War formal international rules were drawn up to standardise national accounting. In 1953 it became a formal UN document called the SNA. This was then updated in 2008.

Any form of fixed value was removed in the SNA and everything based on marginality or value-added. Hence, the document was long and complex. ‘Common sense’ then required adding into that figure estimates for the black economy. Banking which had been seen as an intermediary, merely recycling value, was seen as adding to the GDP. As were financial services. For developed nations GDP became further and further removed from measuring real value.

.jpg/480px-Mariana_Mazzucato_2016_(cropped).jpg)

Mariana Mazzucato calculated that at least 7.5% of the USA GDP based on financial services is pure vapourware and should not be there!

Some of the items added into the GDP became estimates. They were figures based upon financial instruments that were paper rather than reality. How much of developed country GDP is optimistic fiction is difficult to tell. However, the 2008 Banking Crisis became indicative of how far from true ‘common sense’ the SNA has become!

2008: Banking Crisis

In 2007-2008 there was a global financial crisis. This was described as the worst since the Great Depression. This was caused by what was called ‘sub-prime lending’. In other words lending to low-income homebuyers. This had excessive risk-taking by global financial institutions. Or so we were told. The reality was a lot more complex than that.

These sub-prime loans were bundled together into other financial instruments. The bundled packages made them look like ‘AAA loans’ or ‘risk-free loans’. There was a chain of this: with one financial organisation bundling and passing on to another and so on. This was permitted through something called the Glass-Steagell legislation. That legislation didn’t expect the cunning of the predatory lenders!

There were massive government bailouts to try to avert a complete global meltdown. This triggered problems around the world, specifically in Greece, Cyprus and Iceland. There were many bank failures around the world.

Some of the specific problems were later legislatively closed, after the horse had bolted, so to speak. The core parts of the SNA in which countries calculate GDP were only partially addressed. So future somewhat similar failures are possible.

2009: Cryptocurrency

A year after 2008 the Banking Crisis the first cryptocurrency called Bitcoin arrived. Some people thought this would insure them against banking or government problems. However it has more similarities to a Ponzi or Pyramid Scheme. It is therefore dangerous. Yet appealing as the following advert from 2021 suggests! Fiat currencies currently offer minimal growth. Cryptocurrencies offer growth in the hundreds or thousands of percent. Yet there is a saying that if a deal sounds too good to be true, it probably is.

Gareth Murphy, a senior central banking officer for Ireland stated in 2014: ‘Widespread use [of cryptocurrency] would also make it more difficult for statistical agencies to gather data on economic activity, which are used by governments to steer the economy’. In other words, widespread adoption of cryptocurrency would destabilise national economies. This would destabilise the world economy.

Paul Krugman, the winner of the Nobel Memorial Prize in Economic Sciences, has repeated numerous times that it is a bubble that will not last. He links it to Tulip mania. Contract prices for some recently introduced and fashionable tulips reached extraordinarily high levels starting in 1634. They then dramatically collapsed in February 1637. It is generally considered to have been the first recorded speculative or asset bubble in history.

In 2022 cryptocurrency has not collapsed. In one year, in 2021, it multiplied its value against fiat currencies by a factor of four. Collapsed to a factor of two. Up to four again and is now downward again. It is extremely volatile. Like all pyramid and Ponzi schemes, it will eventually collapse.

There is a secondary problem alongside the lack of validity of it being a 'real currency' and that is the off-scale energy used in 'mining' the cryptocurrencies. Unlike printing fiat currency or even mining gold as a reserve, the energy used by the computer farms to mine crypto vastly outweighs its real value and is a liability for the planet.

What Cryptocurrency illustrates as a non-fiat currency is a further step away from the gold standard. It takes the world towards a virtual economy that could make the 2008 banking crisis look like child’s play. But, it is related to the dominant world economic model. Which itself has attributes making it look like a virtual economy that is unsustainable.

Gold again…

Cryptocurrency has problems but we cannot return to gold. There is a limited supply of gold worldwide and it is used for other purposes than just fiat currency reserves. So returning to that, or indeed another nominal fixed asset, as a standard would also have difficulties.

By the end of 2019 nearly half of all gold in the world is in jewellery. Only 14% of it is in use for things like electronics and only 17% is in official gold holdings for countries.

If one adds in all known gold below ground, which is approximately 21% of all known gold, then the amount of gold held as jewellery becomes unstainable.

Gold mining happens in relatively few countries in the world: The top 10 countries mine 85% of all the gold. If the gold standard were still in place potentially China and Russia would have dominance over the USA. Combined they mine over one-quarter of all gold in the world. However, combining North America and Australia then that coalition maintains dominance. It might be interesting to evaluate the new USA / UK / Australia security pact in that light!

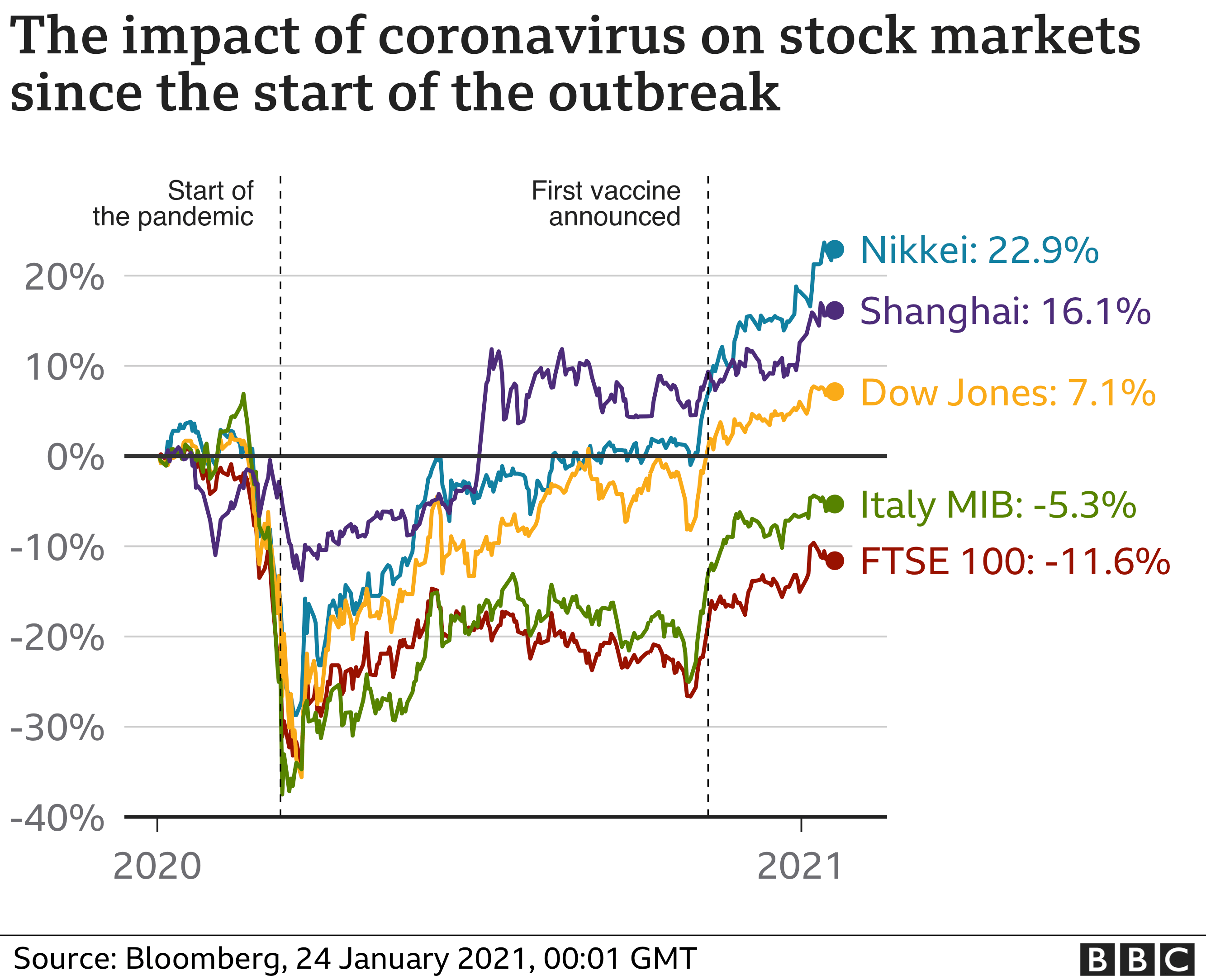

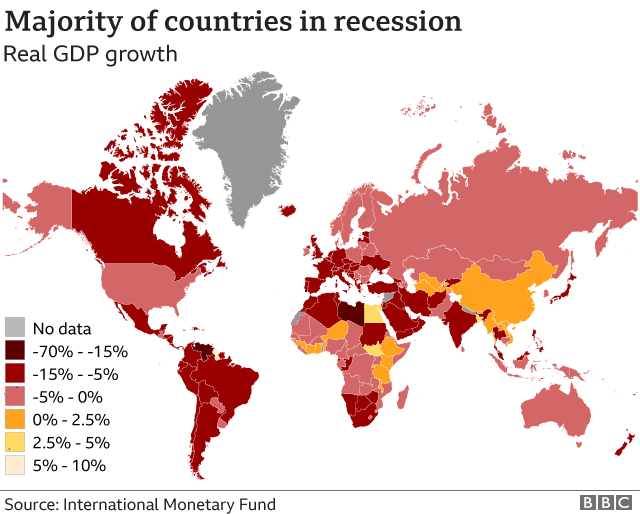

2019: Covid Pandemic

January 2022 and we are entering the third year of the Covid 19 pandemic. There have been over 315 million cases of Covid 19 worldwide and over 5.5 million deaths. Although the number of new cases has risen dramatically over the last two months the number of deaths per day has slightly dropped. Some people are predicting that the end of the pandemic is in sight.

From the start most countries reacted with lockdowns of varying severity. This had a severe effect on their economies. There was a dramatic drop in stock markets. By 2020 the majority of the countries in the world were in a recession.

.jpg/800px-Gita_Gopinath%2C_2012_(cropped).jpg)

* The global decline as the worst since the Great Depression of the 1930s

* The pandemic had plunged the world into a ‘crisis like no other’

* A prolonged outbreak would test the ability of governments and central banks to control the crisis

* Could knock $9 trillion (£7.2 trillion) off global GDP

* The pandemic had plunged the world into a ‘crisis like no other’

* A prolonged outbreak would test the ability of governments and central banks to control the crisis

* Could knock $9 trillion (£7.2 trillion) off global GDP

2021: Climate change

The use of fossil fuels and the plundering of natural resources has been increasing through the 20th century. Recycling is something that has really only been significant for the last two decades. Till recently there was a debate about to what extent climate change was a natural cyclic phenomenon or to what extent it is caused or exacerbated by human activity. Very, very few scientists now rule out the human activity as the primary cause of climate change.

The International Energy Agency publishes the detailed, global energy data but its funders force it behind paywalls. The IEA wants to be at the ‘heart of global dialogue on energy, providing authoritative analysis, data, policy recommendations, and real-world solutions to help countries provide secure and sustainable energy for all’. As it stands the IEA is only providing data to rich elites. The restrictive licenses ensure that it cannot be part of the global dialogue on energy. This charging for the relevant data makes it a tradeable commodity within the global economy. This mitigates against change to the very economic structures causing the damage to the planet!

The IEA data sets are used by governments for economic decision making. Because the IEA data cannot be shared or peer-reviewed the veracity of the data and the credibility of the data cannot be challenged. Academics, journalists and the public at large are excluded from the very dialogue upon which their survival depends!

Non-paywall protected data from the multinational oil and gas company BP is the most commonly used alternative. It is called ‘BP Statistical Review of World Energy’. However, as it is published by a private fossil fuel company it has some obvious drawbacks! It is also very much more limited in scope – with no data at all from low-income countries – unlike the IEA data sets.

87% of annual carbon dioxide emissions come from the energy and industrial sectors. Transitioning to a low-carbon energy system is both critical to the survival of life on earth and urgent. Energy is also a priority for global health and human development. 10% worldwide do not have access to electricity. 41% do not have access to clean fuels for cooking. The estimates of the health burden of anthropogenic outdoor air pollution due to dirty energy range from 4 to over 10 million premature deaths per year.

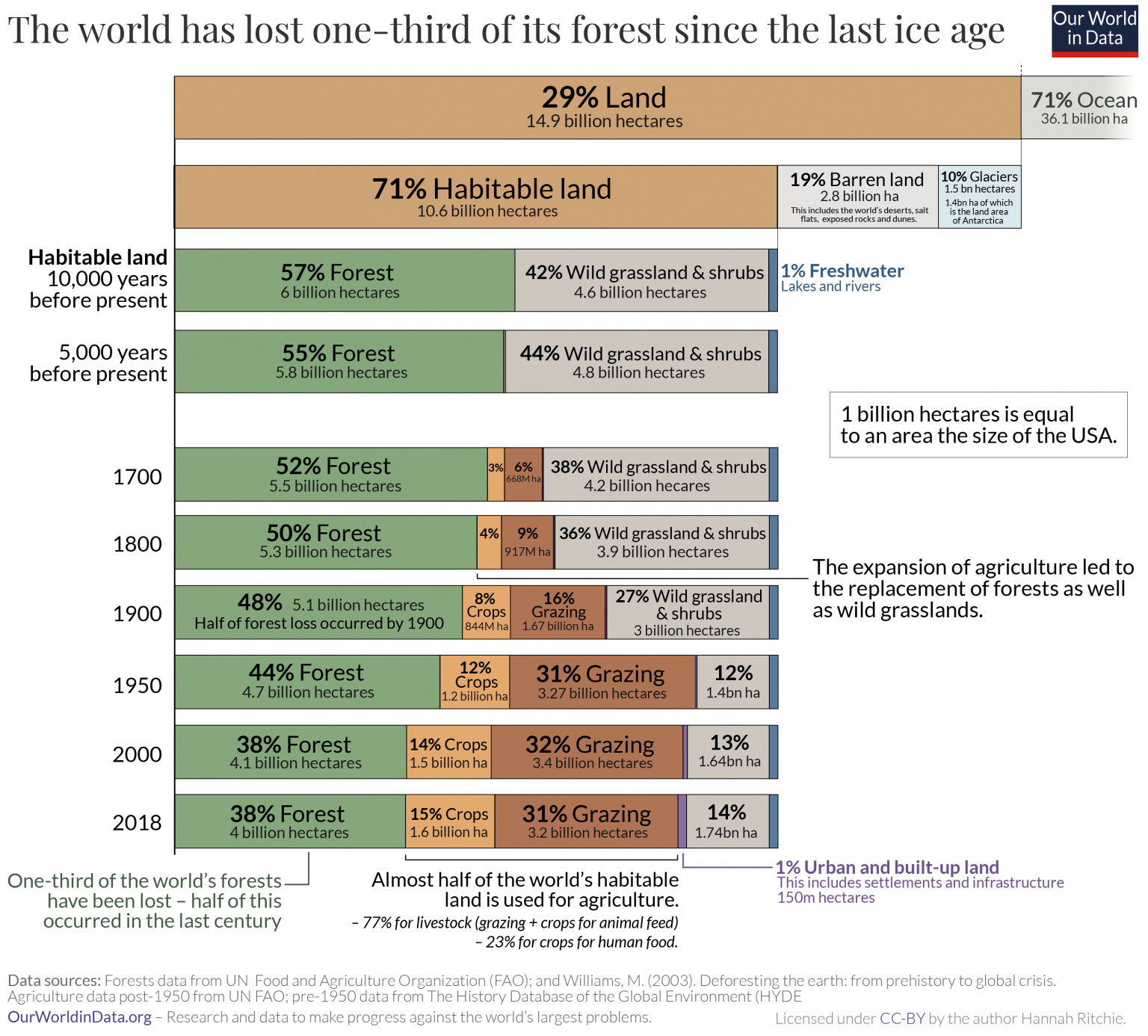

One of the key concerns of the rising greenhouse gases is that they are not being processed due to increasing deforestation.

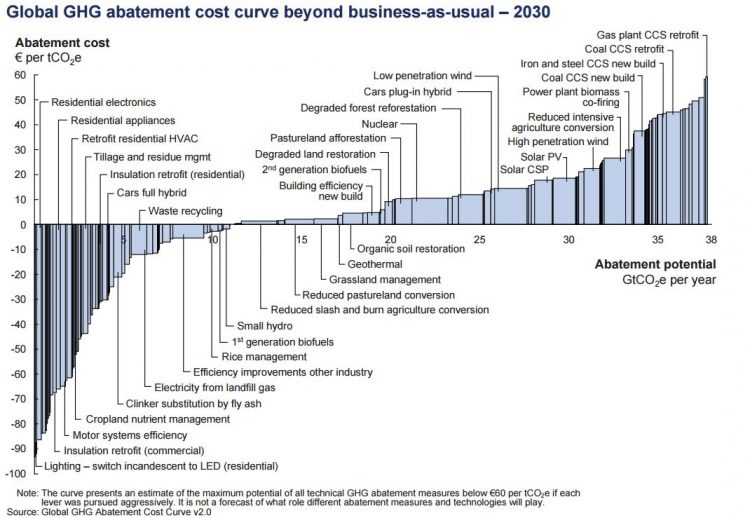

Dealing with the rising CO2 and other greenhouse gas levels in the atmosphere has two issues. 1/ The potential unsustainability of life on earth and 2/ the economic cost of rectifying that. The most common way of measuring and visualising the options and costs of reducing emissions is the ‘abatement cost curve’. This is sometimes called the ‘marginal abatement curve’.

If we aggressively pursue all of the low-cost abatement opportunities currently available, the total global economic cost would be €200-350 billion per year by 2030. This is less than one percent of the forecast global GDP in 2030. But note the validity of the global GDP itself is questionable. However, we can only work on the existing model till a new one replaces it.

The graph is somewhat complicated. The x-axis shows the savings in greenhouse gases which is scaled in GtCO2e (billion metric tonnes of CO2 equivalence).

The y-axis shows the abatement cost in € per tonne of CO2 saved. ‘Cost’ refers to the economic impact (which can be a loss or gain). This is the cost of investing in new technology rather than continuing with existing or ‘business-as-usual’ technologies and policies.

Potential mitigation options are ordered from left-to-right in terms of cost. They get progressively more expensive as we move to the right. The higher the bar, the greater the cost.

2100: Population Plateau

In 1864 during the American Civil War General Sherman made a wartime order to allot 40 acres of land to freed slave families. Plus to lend army mules to help the land reform. This became known as ‘forty acres and a mule’. The size was what was considered a self-sustaining homestead for a family in subsistence agriculture. At that stage the average family size was 5.5. Poorer and black slave families had disproportionately larger families. In 1850 every family in the USA could have been given a 40-acre homestead and (just) fitted into the state of Texas! Today every family in the USA could only have a 20-acre homestead using the entire land-mass of the USA.

Since the Second World War we have seen a huge growth of the world population. This resulted in a concern about overpopulation on the earth. However, the peak of population growth happened in 1968 – close to 50 years ago – and is now declining year on year. Though the population is still growing the rate at which it is growing is slowing dramatically. The world population is predicted to plateau at around 11 billion in 2100, which is 80 years hence.

This affects a number of things: How many people do we need to feed and house and to what extent the number and rate of consumption are increasing? As a closed system, the earth as a biosphere is tending towards its limit. Yet our economic models assume consumers and consumption keep expanding. This is a false premise. As the population plateaus so consumption will plateau. There will be replacement rather than increased consumption and this will need a very different economic model.

Avoiding the Impending Economic Tsunami

In a matter of 12 years – from 2008 to 2020 – there has been a series of short sharp shocks to the world economy. These are potentially foreshocks before a larger seismic event. They have demonstrated the fragility of the current economic model. This cannot stand up to even these sorts of relatively minor blows!

It started with the bursting financial bubbles of 2008. Then added cryptocurrencies that aren’t even paper linked to economic activity. Add to that climate change. Then Covid 19. And consumption will plateau due to a population no longer expanding. We have banking instruments that are virtual and, in some cases, recursively virtual. And the SNA champions those activities. I thus perceive we are heading toward some sort of Impending Economic Tsunami!

Not only are the GDP figures inaccurate but because the model has moved ‘circulation’ and ‘rents’ into ‘production’ the paper financial instruments of the world economy are in reality ‘the emperor’s new clothes’! Though this is particularly true in the developed world it is increasingly so in the developing world.

We live on a biosphere that was a garden and has become a city. As a garden-city we need to look at the economy of the biosphere, not as a ‘continuously expanding pie’ but a ‘fixed-size pie that has to be cut in such a way to allow everyone a slice’. The current economic model is based on the belief in an ever-expanding economy. It cannot function in a globalised world with a relatively static population size and recycling of resources. It won’t work. It cannot work.

We need to look again at the biosphere we call earth, including its human population. We need to develop a new economic model that is based on solid reality not speculative virtual instruments. That model needs to be coherent so that global and national policies are actually implementable.

The Biosphere

The Biosphere we call Earth is (almost) a closed system.

External inputs of energy from the sun, which also creates wind on the surface of the biosphere. There are also potential resources outside the biosphere but vast quantities of energy are needed to gain them so can be ignored at this stage. Solar energy is often referred to as ‘renewable’ but that is a misnomer. It is merely an external source of energy feeding into the closed biosphere system.

The primary inputs are resources found within the biosphere: energy within the biosphere and labour from planet dwellers. The energy comes from everything from (external) solar energy to nuclear energy. The phrase ‘renewable energy’ is a bad one. There is no renewable energy, solar energy is not renewable, it’s just external to the biosphere and continuously available till the sun dies.

The column from Survival up to Luxury indicates values. It closely resembles Maslow’s hierarchy of needs but is based upon values attributed to those needs. There is some overlap between each cell. What Covid 19 has taught us is that if we don’t look out for survival it’s pointless having an economy based on aspiring to luxury! And that is one of the major flaws in the current model.

The recycling column represents outputs that feed into the inputs. For example, only as a person has their survival needs met are they free to labour so the survival recycles to labour input. ‘Virtual resources’ represents the conceptual paper or electronic money we use to gain some inputs. It is dangerous and flawed to see these as anything other than representative documents for physical resources: deposits in a modern gold store if you like. Unless they represent real resources, the Ponzi scheme collapses!

In a closed system with a relatively fixed population, although things wear out and need to be replaced, it isn’t an extra thing that is created but a replacement for an existing something. Thus, the actual number of ‘things’ doesn’t increase.

The losses column represents unusable energy lost and destroyed resources. These have to be minimised, indeed reduced to close to zero, to allow future habitation of the earth. We have already destroyed some resources and converted some energy to heat causing climate change. It is urgent these losses be addressed.

We have a limited but adequate number of resources that we need to care for if we are to survive. Those resources dictate our values. How do we use them? Well, we could, for example, kill two-thirds of the world’s population, as happened in early pandemics, and that would give us significantly more resources for those not killed! It would not solve the climate problem, merely prolong it and it would not change the flawed model the world economy currently uses. A new model is needed based on a closed biosphere system.

The current economic theories/models don’t have as a premise the closed biosphere system that we live on. They will frequently totter on what Malcolm Gladwell accurately describes as a ‘tipping point’. Within such a closed biosphere system those models lead to policies that are incoherent and therefore unimplementable. Unless we change the model, we will certainly be hit by the Economic Tsunami!

Because within the closed biosphere we cannot manufacture wealth out of nothing countries need to see themselves as interdependent, not independent. As do individual human beings. The measure of GDP needs to provide for the Survival and Welfare needs of every person on the planet: A Universal Basic Income (UBI). Where there is a surplus then leisure and luxury can be provided.

Some people have suggested Universal Basic Employment (UBE) to remove the possibility of people just being lazy. The problem with this would be the creation of a multi-class society where the UBE people would potentially be required to work harder and longer than those employed as working weeks became variable with people working fewer hours. This would create an untenable split in society. In places where UBI has been used experimentally, the concern about laziness has been found to be not relevant and not happen. In fact, the opposite has been observed: people will work for the community without compulsion if their income is secure.

UBI doesn’t treat all people as equal but does treat all people as being of equal value. Because the prevailing economic theories are based on the assumption that man is basically self-centred the idea of UBI, people argue, is bound to fail. That premise is not entirely founded on reality and is less prevalent in collectivist cultures than in individualistic ones.

A new SNA would need to be drawn up, where the aim would be not for an ever-increasing GDP but a Global GDP where labour, energy and resources are balanced. And banking and financial services are seen as an intermediary not a wealth creator. It’s not production that has value but humanity itself within a closed biosphere.

Doughnut Economic Model

Doughnut Economics gives a measurement tool for ecological and social foundations and develops the core concept of a closed system biosphere. It is based on the premise of Kate Raworth that 'A healthy economy should be designed to thrive, not grow.'

.jpg/423px-Kate_Raworth%2C_2018_(cropped).jpg) |

| Kate Raworth |

Kate Raworth is author of Doughnut Economics and Senior Associate at Oxford University’s Environmental Change Institute and a Professor of Practice at Amsterdam University of Applied Sciences. In 2021, Raworth was appointed to the World Health Organization's Council on the Economics of Health For All, chaired by Mariana Mazzucato.

Instead of focusing on the growth of the economy, she focuses on a model where there can be ensured that everyone on Earth has access to their basic needs, such as adequate food and education, while not limiting opportunities for future generations by protecting our Ecosystem.

'The Doughnut consists of two concentric rings: a social foundation, to ensure that no one is left falling short on life’s essentials, and an ecological ceiling, to ensure that humanity does not collectively overshoot the planetary boundaries that protect Earth's life-supporting systems. Between these two sets of boundaries lies a doughnut-shaped space that is both ecologically safe and socially just: a space in which humanity can thrive.' (https://doughnuteconomics.org)

The tool was then used by other '21st-century economists' rejecting the Neoclassical Economic Model to analyse where we are and make decisions on the best way forward for a 'safe and just space for humanity'.

The interactive version of this can be found here:

There is one possibility for the closed system biosphere not being the planetary boundary and that is if mining and other heavy manufacturing can be done off-planet - for example on the moon. It has been suggested that this could be possible by the end of the century. Personally, I'm sceptical. Even if it is, then we still need to plan for the next century the biosphere being a closed system. We cannot risk our whole existence on a very risky and potentially impossible hope! Within policy implementation planning there is a key concept of 'no assumptions' and this is an assumption that should not be written into the plan forward.

Richard J Fairhead

January 2022

[Some of the Economic Modelling comes from Mariana Mazzucato’s book ‘The Value of Everything: Making and Taking in the Global Economy’, which I highly recommend reading. Also 'Doughnut Economics: Seven Ways to Think Like a 21st-Century Economist' by Kate Raworth.]

Comments

Post a Comment